Kalpen Parekh is the Managing Director, Sales &

Marketing at IDFC Asset Management Company Limited and has over 14 years

experience in Retail Sales & Distribution.

He has been associated with IDFC AMC since December

2010. Prior to joining IDFC AMC, he was associated with Birla Sun Life AMC, as

Head - Sales & Distribution and earlier was with ICICI Prudential AMC as

Joint Head – Retail Sales & Distribution.

He holds a Masters Degree in Management Studies

in Finance and a Bachelors Degree in Engineering (Chemical). Kalpen comprehensively

answers my questions on the changes at IDFC AMC and the strategy

followed for some of its schemes.

Hi Kalpen!

Was great meeting you at Chennai. Your efforts to upgrade advisor skills

through various programs and behavioural sessions and the tools you have

provided have been much appreciated. Thank you for taking time to answer some

of my questions.

There has been a major change in the Fund

Management team of IDFC, with the moving out of Kenneth Andrade and Punam Sharma.

Anoop Bhaskar has taken over. Can you give some details on the fund management

team now at IDFC?

Thanks for

the opportunity to talk to your investors.

We have

gone through a transition over the last one year!

Punam and

Kenneth were part of the team which set up the equity platform and helped us

reach our current scale of 10000 cr Equity AUM

Over the

last one year, not only has Anoop joined us but we also have significantly

strengthened the team further – We have added one analyst and three fund managers

on the equity side. We have now built the team keeping in mind our future

growth aspirations.

How has the transition been after a fund

manager change? What has been your initial focus?

Our focus

over the last year was to give confidence to our investors and advisors that

they are a part of an Institution which is able to attract talent and can

manage long term assets. We have ensured we have built a high quality team with

all the hiring done now as mentioned above.

We have

ensured continuity in the way we manage money in our flagship Fund Premier

which is a very unique fund. To a consumer/investor, it’s a fund which has

stood for Experience because of its investor friendly design of being an SIP

fund always and opening it up for larger investments when we see compelling

investment opportunities for the medium term.

We have

used this transition to reinforce and communicate our investment process and

investment framework for every fund of ours! Our focus is to make our investors

aware of what each fund stands for over and above its performance as an

outcome.

We

recognise that IDFC Sterling and IDFC Premier are better known Product Brands

from IDFC MF platform and we need to complete our product gap in the Large Cap

and Diversified segment hence we have also invested in revamping Classic and

communicating extensively about Classic as a credible product in the Diversified

Equity Segment.

I have seen a lot of changes in your Classic

Equity Fund and a pickup in its recent performance. Would you like to share

details on the process/changes you have made in managing this scheme?

IDFC

Classic Equity fund has been revamped this year to take a new avatar that

follows a “Quality & Relative Valuation” framework.

The focus of the fund is on quality

companies, mainly from the balance sheet perspective. A three factor model focusing on

the following attributes will help filter companies for this investment

strategy.

A. Cash

generation from operations as a percentage of EBIDTA;

B. Debt

repayment ability (Debt / EBIDTA < 3)

C. Profitability of the business (RoE of 15% over a business cycle)

C. Profitability of the business (RoE of 15% over a business cycle)

Companies which qualify on the above

parameters will then be classified into sectors. The

final selection would be driven by relatively lower valuation of the

identified companies within each sector on P/BV (Price to Book Value)

basis.Such identified companies would comprise between 50-65% of the portfolio.

Allocation to financials would be between 25-30% and the balance would be theme

driven / high quality companies.

This strategy of purchasing quality companies

with sufficient margin of safety has resulted in lower PE and PB for the fund

as compared to Nifty. This gives us comfort given the current market valuations

are on the higher side and can limit downside in case the expensively valued

stocks correct.

You mentioned that you will have a 25-30% allocation

to financials in Classic Equity?

IDFC Classic Equity Fund will be conscious of

the benchmark (S&P BSE 200), and therefore will maintain similar weights

towards the sector. Currently the fund has ~27% exposure to the Finance space

(in line with the 29% exposure of the benchmark).

Any changes in your approach towards the

Iconic Premier Equity Fund?

We continue to re-emphasize the key

attributes which have been the driver of the long term performance delivered by

the fund during its first decade of existence. Buying ‘Quality’ companies, a

key attribute, which has been critical for the fund’s past performance is now

being detailed on the following factors: 1. High promoter holding; 2. Higher

than sector profit growth over the medium term; 3. Improving trend of RoE; 4.

Low leverage and 5. Generating free cash flow.

IDFC Premier Equity Fund further has added a

new element (Sell Discipline) to give the fund an extra dimension to sustain

the strong long term performance.

The Sell discipline - PEG ratio of 3x+ for 2

year forward earnings estimates, will help us trim/exit stocks where valuations

appear to have moved ahead of actual performance.

In my view, what’s made Premier iconic is the

experience to every investor – those who continue their long term SIPs as well

as those who invested whenever we have raised new money by opening the fund

selectively. We would continue with this approach for Premier.

Any changes envisaged in your midcap scheme,

Sterling Equity?

We will incorporate a ‘core portfolio’ concept comprising 25-35 stocks which will form

the foundation of the portfolio for the future. Our stock selection would

balance growth aspirations with balance sheet strength. We would remain sector

agnostic, with focus on individual companies.

The near term focus would remain on

valuations than future growth expectations; this may lead to portfolio changes over the next few quarters in

Sterling Equity. Over the medium term, portfolio churn will be a key metric

of focus. We aim to significantly improve on this metric going forward, aided

by the incorporation of ‘core portfolio’ concept.

The fund is currently over weight Auto,

Consumer Discretionary and Industrials. We plan to increase weight in

Financials stocks and maintain or reduce weight in IT services on account of

higher valuations.

Do you have any new products or NFOs in mind?

How do you wish to drive the growth at IDFC MF?

Our growth will be via balance of new ideas and scaling

existing products across Debt and Equity.

A

lot of our fixed income funds have delivered credible performance and alpha

over the last 3 to 5 years, without taking excess risk. India is an FD market

and there is a large opportunity to position various short term funds as a

replacement to Fixed Deposits. We have a range of funds in this segment managed

both passively and actively.

I

see a large opportunity for asset allocation funds to grow in the near term as

both Equity and Debt have delivered good returns and funds which allow us to

manage both asset classes actively can be good ideas for incremental

investments – we will scale our Asset Allocation Funds and Dynamic Equity Fund

in the coming months

We have filed for a Balanced and Credit opportunities

Fund and we are awaiting SEBI Approvals

You’ve been known to come up with ideas to

improve investor experience like the PE Ruler / traffic signals and have lately

mentioned PE STP. Can you elaborate a bit for readers on how this works?

We all

know that Equity in the long term generates Wealth but in the short Term

generates Volatility. Thus, without Volatility, Wealth Creation is an illusion.

Our PE Scale

was the first attempt by an AMC to upfront show to investors both the sides of

Equity as an Asset Class.

Evidence

shows, that while Mutual Funds NAVs grow over decades, it’s not the same in

investors’ account statement, especially as investors tend to invest for

shorter time horizons. 80 pc of equity flows come when markets are richly valued

and on the basis of past performance and as the market cycle turns; investors

get disappointed with early volatility.

Thus, PE Scale upfront

states that volatility can’t be avoided; but if one is aware, it can be

managed. It also tells investors, that the worst time to exit Equity is in

Green and Yellow Zone, when the foundation of future returns is being laid out

While the

PE Scale became popular, we got feedback - why not design funds or processes

which can apply the principles for them in an easy manner. That led us to

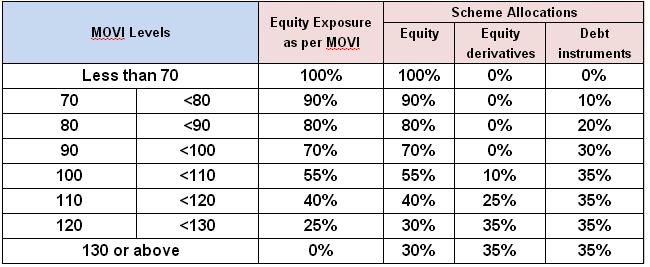

launch Dynamic Equity Fund, which increases Equity exposure in Green Zone and

reduces it in the Red Zone thus cushioning volatility. For eg, in the last two years

since launch, it has outperformed Nifty with an average 55% exposure to Equity

Likewise,

we got the idea to launch PE STP. When PEs are high, many investors stagger

their investments via STP (Systematic Transfer Plan). What we realised, is that

most STPs had a short tenor of few months. An STP becomes a lumpsum actually if done in

short tenors.

PE STP

increases the investment transferred to Equity in Green by 5 times and 2 times

in Yellow Zone and maintains the instalment amount in the red zone. Thus it

follows the basic rule of good investing – Invest more when markets are cheap

and less when expensive. Evidence shows that this approach reduces purchase

price and increases probability of outperformance

PE STP is

an idea which allows investors to earn excess returns via a scientific process

and discipline.

A candid question! Do you and your fund

managers invest in the funds you manage?

I have

been with IDFC Since 2010. 100 pc of my investments are in IDFC MF

since then. I have invested in IDFC Premier, Sterling, Classic, Dynamic Equity,

Dynamic Bond, Arbitrage fund and All Seasons Bond Fund

Likewise

all our colleagues across functions invest in our own Funds.

Thank you

Kalpen. Wishing you and the team at IDFC AMC a Happy Vijayadashami and success

in all endeavours.